State of Food Manufacturing: Period of Polarization Emerges

Polarization characterizes the production forecasts, capital spending plans and structural positioning taking place within America's food and beverage plants, based on the results of the 26th Annual Food Engineering State of Food Manufacturing Survey.

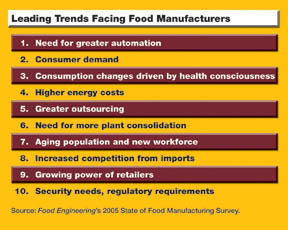

Outsourcing is a macro trend cutting across all types of manufacturing, and the 224 respondents to this year's survey confirm it's a growing fact of life. In fact, the trend is accelerating: 26% of respondents indicate outsourcing at their companies increased in the last year. Two years ago, only 13% indicated outsourcing was on the rise.

At the same time, 16% say in-house engineering staffs are being beefed up at their firms-double the proportion of companies two years ago. Conversely, the proportion of processors downsizing engineering staffs declined slightly to 13%. These trends suggest two divergent organizational approaches: stripped down staffing on one hand, and a greater commitment to proprietary expertise on the other.

The same feast or famine dichotomy is reflected in current capital budgets. Four survey questions asked production professionals to indicate spending trends in control equipment, maintenance automation and other areas. In all cases, the proportion who say spending is unchanged from the previous year is the lowest in five years. Most find themselves with more automation dollars than in the past. But higher proportions also report reduced budgets than in recent years.

Spending for production, packaging and process control equipment is the most robust automation capital area, with more than two fifths of respondents indicating bigger budgets. The average spending boost is 17%. At the same time, 15% say spending in this area is down by an average of 22%. A year ago, 11% indicated cuts in this area.

Higher proportions of plants are investing in more automation and control hardware and software and in more maintenance-related automation than in previous years. Maintenance spending is particularly bullish, with a third of respondents reporting average budget increases of 11%. A year ago, only 28% of companies boosted spending in this area, and the average increase was only 8%. The proportion of companies cutting spending nudged ahead to one in 10, though the cuts are draconian: 24% on average, up from 18% last year.

Budgets for plant improvements and upgrades are taking a hit. The proportion of those planning to spend more slipped to 35%, and their additional budgetary dollars are up an anemic 18%, compared to 2004's 28% boost. At the same time, those experiencing budget cuts spiked to one in five, up from 11%. The average spending cut is 22%, a little less severe than last year's 25% average cut.

Consolidation's consequences

Since bottoming out in 2002, merger and acquisition (M&A) activity in the food and beverage industry has staged a modest rally, with early indications that this could be the most bullish year since 2001, according to The Food Institute, based in Elmwood Park, NJ (see chart at right). Last year's activity would have been on par with 2003 if several announced deals had closed, including the largest: Wm. Wrigley Jr. Co.'s $1.46 billion purchase of Kraft Food's Life Saver and Altoids business. The confectionery deal was completed this June.

For those impacted by mergers or consolidation, the greatest impact remains consolidation of manufacturing into fewer locations. Integration of ERP and manufacturing information systems leaped to number 2 on the impact list, with almost half of respondents citing systems integration as a major challenge, up from 35% the previous year. Divestiture of selected operations was mentioned as a challenge by 30%, up from 24%. Reassignment of manufacturing management was pinpointed by 37%, down 10 points from 2004.

Efforts to improve supply chain efficiencies appear to be paying off. Software is being implemented to improve supply chain integration at two out of five respondents' firms, up from one in four a year ago. Fewer than one in five manufacturers are doing little or nothing to better integrate the chain, half the head-in-the-sand rate of a year ago. Apparently, many managers feel there is little room for greater improvement: one third say there isn't a need for better supply chain management to improve productivity, while only one in eight believe there is a great need for further improvement, one-third less than the number who put a high priority on this a year ago.

In the area of customer relations, food companies have moved aggressively from the talking to the implementing stage on several fronts. Half the companies now provide customers with Web-enabled access to purchase order status and other information, double the number of a year ago. Web portals are in place for a third of respondents' customers and suppliers to place orders and provide feedback, up from only 13% a year ago. Two-fifths are using EDI to capture orders and forward invoices, up from a quarter in 2004. Implementation or investigation of RFID tags is occurring at 36% of the companies, up from 22%.

Programmable logic controllers continue to top process control shopping lists, though it slipped slightly to 83% of respondents. HMI screens are on the buy lists of two-fifths of companies, up 10 points, and distributed control systems or DCS expansions are planned by a third, more than double 2004's rate. Software for statistical process control, integration, supply chain management and energy management all exhibit strong purchase-intent gains.

Managers continue to beef up plant security, with closed-circuit cameras, surveillance systems and raw-material protection measures cited by respondents as some of the steps their organizations are taking. Building and perimeter security has been tightened at 87% of the plants, up from 79% a year ago. Personnel screening was being done at three-fifths of the companies two years ago; today, three-quarters of the firms have programs in place. In fact, respondents indicate increased attention across the board in operational security.

However, food professionals may have a blinkered view. A basic requirement of the Bioterrorism Act is the registration of all domestic food manufacturing facilities, as well as all foreign plants producing food and beverages for export to the US. The FDA conservatively estimates there are 200,000 US food plants and 200,000 foreign exporters. As of mid-September 2005, only 116,407 US plants and 151,658 foreign facilities had registered. The deadline was December 2003.

Given the black or white nature of registration-a plant is either fully compliant or out of compliance on this score-a sliding scale isn't necessary. Nonetheless, only 5% of respondents admit they are out of compliance, 50% say they are fully compliant, and the other 45% suggest they are somewhere in between. Presumably, a committee is studying the registration form and will get back to the FDA soon.

Help wanted: tomorrow's engineers

With a significant portion of today's food engineers making plans for their golden years, America's food and beverage plants will have a serious staffing challenge in the near future. Where will the industry find their replacements, what skills are most in demand, and what training programs are being developed to cope with the looming engineering brain drain?According to respondents to this year's State of Food Manufacturing survey, mechanical engineering is the most critical skill set, closely followed by electrical and chemical engineering. Electronics, industrial and process engineers also are in high demand. Where people say those specialists will come from depends on who is answering the question.

Colleges and offshore locations will be the primary sources, if the prevailing view among respondents is correct. "Our engineers come from major US universities and India, in about equal proportions," one professional writes. "Companies must recruit graduates and train them" before their experienced engineers retire, adds another. "The [critical] skill is simply integrity."

On-the-job training and internships also will play a role. "Hands-on repairs for maintenance engineers [not just books]" will help address the need, one individual writes. "Training is available, but most engineers don't put out the effort to apply their learning." Mentoring programs pose another opportunity. "Replacements need basic education, and then they need to learn from the experienced engineers," a respondent writes.

"We just plan to develop young engineers from school and put them through a training process that our company is developing right now," explains one person.

Pessimism is reflected in the comments from some. "Nothing is being done to prepare," one professional writes. "Electrical engineers, software and mechanical engineers will be needed" and be "most sought after," yet "no one is developing training." Supplier assistance would be a welcome assist, he adds.

Contract services and other outsourcing will become bigger factors, many believe. One respondent sees an opportunity with senior citizens who want to keep their hands and minds engaged. "We are using retirees on a consultant basis," tapping their expertise in "project management skills, on-the-job training," this professional writes.

Some are putting their faith in bright, young minds that can be molded to meet the rigors of plant engineering through training in Six Sigma and other disciplined approaches. "Young management trainees will go into engineering," one confidently predicts. "Mechanical and electrical engineers are always in demand."

Memo to boss: can we talk?

Better communication at all levels may be the most pressing need at today's food firms, based on responses to an open-ended question asking respondents where their companies' manufacturing missions fall short.More automation, increased flexibility and a greater commitment to capital improvements received their due, but soft issues like communication, teamwork and employee morale are uppermost in the minds of many participants in this year's State of Food Manufacturing survey. "Better communication skills with consumers and employees," writes one respondent, reflecting the view of scores of participants. "Continuous improvement and communications in the benchmarking process," summarizes another.

Better training is another pressing need. "Employee performance accountability, more exclusive training and holding employees responsible" are needed to fill the mission gap, a respondent writes. "Equipment, personnel skills, better training and selection," offers another.

Best practices and more standardization are emerging as key issues, whether standardization involves systems, multiple plants within an organization or implementation of lean manufacturing or Six Sigma principles. Some respondents make a direct correlation between better product quality and improved communication and information transparency.

Summarizing common sentiments, one respondent cites "outdated operating and quality procedures and increased internal training to create more training-the-trainer" programs as his organization's pressing concerns.

Dietary concerns and food manufacture

Public awareness of healthy living will have as much impact as automation imperatives on manufacturing operations over the next five years, if survey respondents are correct.Asked to cite the top two trends that will impact food processing, food professionals were as apt to name external forces as trends in manufacturing. And healthier eating and drinking far and away will be the biggest shaper of what gets processed and how. "Health and wellness trends will require new formulations, causing significant process changes," one professional writes. "People are eating/drinking healthier," another writes. "Water is the largest growing market for my company."

A growth in imports also is seen as a macro trend that will impact US manufacturers. Radio frequency technology, Six Sigma and the growing power of mega-retailers are uppermost in the minds of many.

Bioterrorism concerns manifest themselves in several ways. Supplier security protocols, regulatory oversight and the safety of employees all are impacted. "Tighter security; cherish employees," one respondent writes.

Rising energy costs are top-of-mind for many. Despite all the distractions, many remain focused on fundamental issues such as lean manufacturing and better process control. A "high-performance work system" based on a team concept and "process control automation" are the top areas of focus for one respondent.

Who answered the survey

A combination of mailed surveys and outbound telephone calls generated the 224 useable responses to this year's State of Food Manufacturing survey. The 8% response mail response rate was consistent with previous surveys. Telephone surveys generated a 17% response rate.Job diversity defines this year's respondent profile. Half the surveys were completed by food professionals in operations management (27%) and engineering (24%). Production managers provided one in five responses, general administrators accounted for 13%, and the balance came from professionals in the areas of R&D, quality control, purchasing, packaging and other disciplines.

The views of a broad spectrum of food and beverage processors are represented in the survey. Meat processors and beverage companies are the largest segments at 23% each, followed by bakery (20%), dairy (19%) and flavors/food ingredients (14%). One-third of respondents work at facilities with 500 or more employees, another third at plants with 100-249, a fifth at facilities with 250-499 and one in 10 at plants with less than 100 workers.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!