Replacement Parts & Components Trends Survey

14th Annual Replacement Parts Survey: Proactive inventory practices

Survey shows processors are increasingly using technology to take a closer look at inventory management.

Food Engineering’s 2016 Replacement Parts and Components Trends Survey identifies the “who, what, why and how” of replacement parts purchasing, inventory maintenance, condition monitoring and related topics. The key objectives of the survey are to identify the type of job functions involved in replacement parts and components decisions; replacement parts and components industry professionals rely on; the most important factors when selecting a supplier; and maintenance replacement and inventory management strategies that are currently utilized. In the survey, nearly half of the polled food and beverage manufacturing personnel reported spending less on replacement parts and components in 2015 than in the previous year, with the median spend decreasing from $300,000 to $100,000. The mean expenditure also fell from $1,136,249 in 2014 to $866,426 last year—a 24 percent decrease.

Article Index

- ROI and OEM

- Product quality and availability

- Automated ordering and delivery services

- Balancing costs and reducing downtime

- Sidebar: About the Survey

The number of respondents to this year’s survey who spent less than $100,000 on replacement parts increased to 48 percent (vs. 32 percent in 2014); 25 percent reported spending between $100,000-500,000. The number who spent between $500,000-1,000,000 declined to 11 percent from 14 percent the previous year, while those spending between $1,000,000-5,000,000 fell from 25 percent in 2014 to 14 percent in 2015.

As in previous surveys, maintenance personnel were most frequently involved in the majority of maintenance decisions. General administration/executive management was the second-most involved group in these decisions (23 percent).

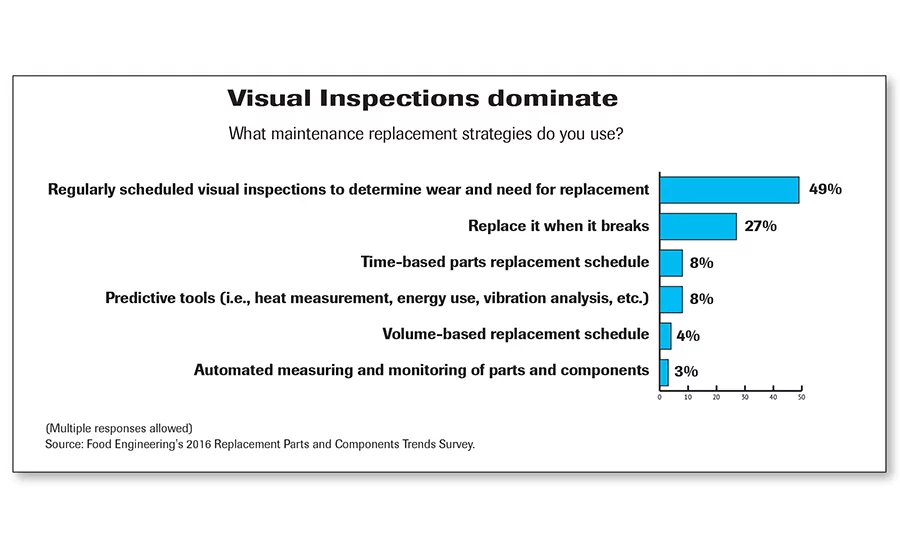

Regularly scheduled visual inspections as a maintenance replacement strategy continued to dominate other methods, rising to 49 percent, with “replace it when it breaks” coming in at 27 percent.

The number of respondents using time-based parts replacement schedules fell to 8 percent from 2014’s 12 percent; those applying predictive tools as a maintenance replacement strategy also fell from 10 to 8 percent. The use of volume-based replacement schedules and the automated measuring of parts and components slightly rose, to 4 percent and 3 percent, respectively.

ROI and OEM

Half of this year’s survey respondents said they have quantified maintenance costs and can calculate the ROI of the higher quality parts. Thirty-one percent said most parts are commodities, with price the determining factor when specifying replacements, as opposed to 46 percent in 2014. Twelve percent indicated manpower shortages forced them to choose the highest quality parts vs. 14 percent in the 2015 survey.

According to the current survey, 10 percent of companies use only high-quality OEM parts at their facilities. Among respondents who have used less expensive parts, 47 percent reported experiencing premature machine failures; 41 percent said less expensive parts do not work as well as the higher priced versions. However, 31 percent said the less expensive parts work just as well, and 26 percent reported having no problems with non-OEM parts.

Bucking a previous trend, more respondents this year said they received parts that may have been counterfeit; 9 percent confirmed this, compared to only 3 percent in the previous survey. However, only 1 percent reported having other issues with non-OEM parts, way down from the 10 percent in the 2015 survey.

Product quality and availability

Product quality remains the most important factor when selecting a replacement parts and components supplier, cited by 97 percent of the respondents. Ninety-four and 92 percent, respectively, highly value product availability and on-time delivery, which corresponds to the trend of seeking solutions to reduce unscheduled downtime due to equipment failure.

Ninety-two percent of the respondents said value for price paid is also highly important, while 76 percent cited technical service support. The importance of product warranty edged out company reputation in the rankings, at 72 percent and 63 percent, respectively.

When it comes to choosing a supplier, having a previous relationship is important to half of the respondents, while the availability of electronic ordering and order tracking is a major factor for only 45 percent. Forty-one percent ranked lowest price as a top supplier characteristic. Product line breadth and national or global service capabilities were also cited as important supplier characteristics by 39 and 32 percent of the respondents, respectively.

In this year’s survey, about one-third of the respondents said they have not changed their parts management in the past two years. However, those that have made changes improved their inventory management or added personnel. Many of the answers reflect that companies are using technology to take a closer look at inventory management, such as one respondent’s comment that the company “moved from a mix of online and manual systems to all being computerized and tracked on SAP inventory [systems].”

Another respondent said the implementation of a computerized maintenance management system (CMMS) increased efficiency of the maintenance department and “filtered through to operations, resulting in an increase in operational efficiency due to fewer maintenance breakdowns.” Many of the companies reported hiring more personnel to manage their parts. According to one respondent, “We decided to designate half of the responsibilities to two different associates, [resulting in a] much smoother process.”

Automated ordering and delivery services

While one in three respondents reported having no automated parts ordering process, those that do (22 percent) most commonly use system-generated purchase orders. Nineteen percent use a CMMS. Another 13 percent use standardized hard copy purchase orders, while 10 percent reported using a direct-data link to a parts supplier or distributor.

Balancing costs and reducing downtime

Most respondents (60 percent) reported making no changes to their inventory practices in the last year. Those who made changes were more likely to have reduced their replacement parts inventory (27 percent compared to 20 percent in 2014). Only 13 percent increased their inventory. Overall cost reduction was the main driver for decreasing inventory. Other reasons include the elimination of old and/or obsolete inventory, as well as moving to just-in-time practices. For instance, one respondent stated, “We have found we should only keep replacement parts for items that are difficult to find or ship from far away.”

Among those who have increased their inventory, most said they added more equipment, as well, and now stock more critical parts in an effort to reduce downtime. As one respondent explained, “The increases in product output vs. demand from customers requires equipment to have minimal downtime, [so] the facility built in a parts inventory program to minimize downtime.”

Approximately 40 percent of respondents said they have implemented maintenance repair operations (MRO) cost-cutting strategies. Improving inventory management was the most commonly employed method, followed by predictive or preventive maintenance. Additional strategies reported include vendor-managed inventory programs and standardizing equipment and parts across the plants.

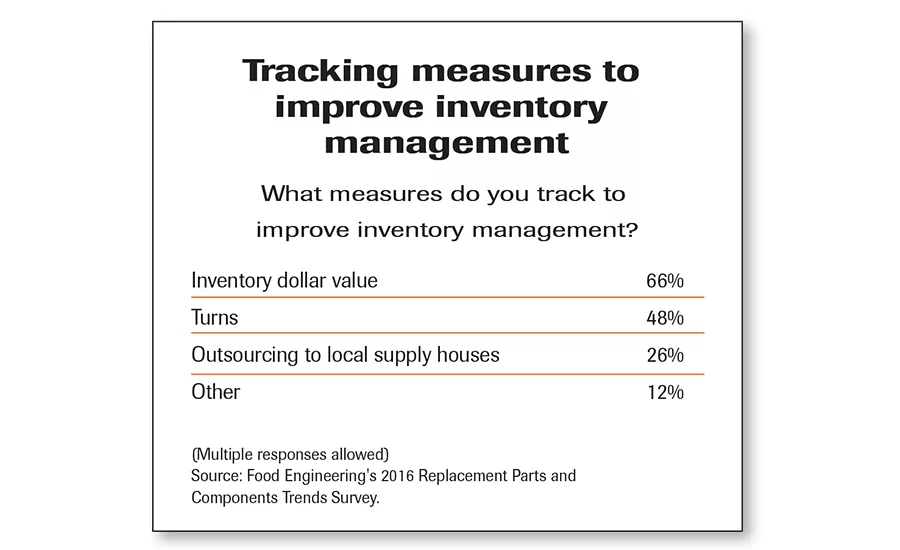

Sixty-six percent of respondents said inventory dollar value is the most used method for improving inventory management; 48 percent use turns. Twenty-six percent said they have outsourced inventory management to local supply houses. According to 25 percent of the respondents, the greatest challenge to minimizing inventory is the lack of funding to organize and streamline inventory practices. Another 25 percent stated multiple sourcing options for ordering parts present a challenge. Fifteen percent reported the absence of a searchable parts database is a major obstacle to minimizing inventory, while 11 percent said the lack of consistency in the names of parts causes problems.

Among the respondents using condition-monitoring tools, vibration analyzers are most popular (used by 45 percent). Following closely behind are thermal imaging (used by 42 percent) and infrared sensors (41 percent). Oil analyzers, ultrasonic sensors and stethoscopes are used by 33, 22 and 15 percent of respondents, respectively. Approximately one-third of respondents reported not using any condition-monitoring tools.

About the survey

The report’s statistics and comments reflect the responses of Food Engineering readers who returned mailed questionnaires or elected to complete the replacement parts survey online. General administrative/executive management, engineering personnel and plant operations professionals represent 74 percent of respondents (32, 22 and 20 percent, respectively). The remaining 26 percent of respondents are split between research and development (10 percent), maintenance (6 percent), quality assurance/quality control (6 percent), purchasing (3 percent) and other (1 percent).

Fifty-four percent work for a company with less than 100 employees, while 25 percent work at a company with between 100-499 employees. Eleven percent are from a company with more than 1,000 employees, and 10 percent work for a company with 500-999 employees.

The primary products produced by 15 percent of respondents are bakery and snack foods, while 12 percent produce beverage products, and another 12 percent produce processed meat, poultry and seafood products. Ten percent produce candy, sugar and confectionery products, while 8 percent are co-packers or co-manufacturers of food and beverage products. Eight percent of respondents are from corporate or divisional headquarters, 8 percent produce dairy and frozen novelty products, and an additional 8 percent produce frozen food and prepared meals/fruits and vegetables. Another 8 percent produce dietary products, chemicals and food ingredient products; 7 percent produce cereal and grain-based products; and the final 5 percent produce shelf-stable foods or soups, sauces, jams and jellies.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!