Market Trends

Food industry to face downside risks this year

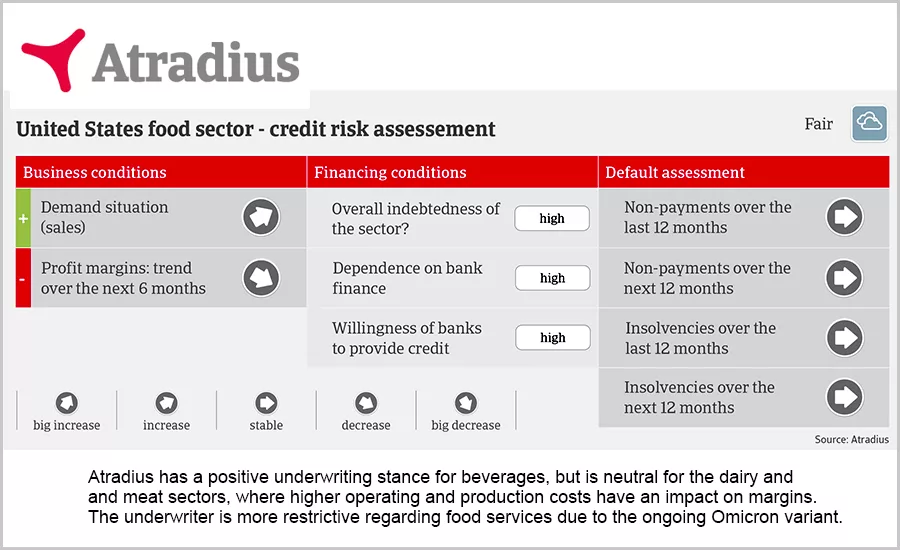

According to global credit insurer, Atradius, challenges in the U.S. include rising commodity, energy, labor and transport costs

A number of downside risks are expected to pose major challenges to the global food and beverages sector this year, according to the global credit insurer Atradius in its latest “Food & Beverages Industry Trends” report.

Sharp increases in commodity and energy prices, labor shortages, transport issues and the ongoing spread of the coronavirus pandemic could jeopardize the profitability of major industry subsectors over the coming months. In addition, consumer habits are changing as the end-client increasingly demands full transparency about their ingredients, production processes, and supply chain. All this could subsequently strain profit margins within a fiercely competitive industry, where the bargaining power of major retailers and discounters is very strong.

However, the global food and beverages industry has various drivers that can unlock potential growth this year. These are the non-cyclical nature of the industry, a growing number of middle-income consumers in emerging economies who are spending more money on high than low value-added goods and the increasing use of technology to engineer solutions for global food supply are all contributing to growth. However, these factors could highly likely turn the surge in demand into a snack rather than a full meal, says the report.

Variations among the countries covered in the report, ranging from Australia, Canada, Indonesia, many European countries and the US are wide and businesses should be aware of this in their regular trade activities with the industry.

In the U.S.

U.S. food and beverages value-added output is forecast to grow by about 1% in 2022, after increasing 3.1% in 2021 and 1.8% in 2020, says the report. The food retail segment benefited from higher sales over the past 24 months, but competition remains fierce and margins tight. In the food services segment a rebound is underway, but many businesses still struggle to absorb the sharp decrease in demand from hospitality seen in 2020 and the first half of 2021. The current spread of the Omicron variant remains a downside risk for the ongoing recovery.

U.S. production costs have increased across all subsectors, due surging prices for commodities, transportation bottlenecks and labor shortage, says the report. Additionally, droughts in central and western states could adversely affect production and margins in the fruit and vegetables subsector. While the margins of food producers and processors have been adversely affected by higher input costs, both are in general able to pass on a large share of those costs to wholesalers/retailers and end-customers. This has resulted in the highest food price inflation since 2008 (up 6.3% year-on-year in December 2021). Atradius expects that food prices will remain elevated until supply constraints ease in the second half of 2022.

Access to financing is not an issue for food and beverage processors, according to the report. Many are private equity-owned and, therefore, highly leveraged, using credit lines for working capital. Ongoing mergers and acquisitions in the industry are also a reason for high department levels. Next to food retail, Atradius’ underwriting stance is open for beverages, as most businesses I this segment show a solid performance and sufficient liquidity.

For more information and to download the report for free, visit https://atradius.us/reports/food-industry-trends-united-states-2022.html.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!