COVID & Inflation

COVID cases drop in the U.S. while food prices climb

A new study finds diminished worry about COVID among American consumers, but an overly heightened concern about food price increases

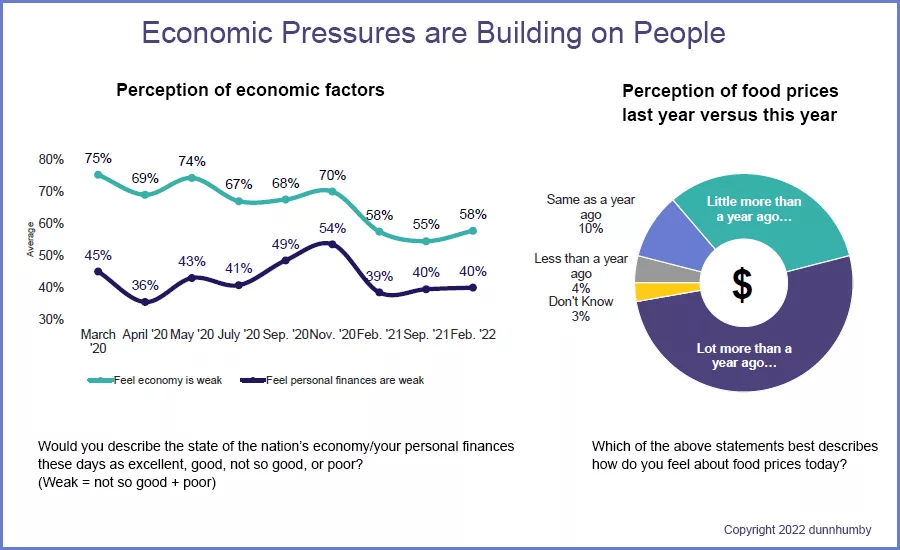

After starting to recover, people are now more concerned with their finances and the country’s economy than they were a few months ago. Most notable: 83% think food prices have gone up and half say they have gone up a lot. Graphs used by permission; © dunnhumby 2022

A recent study from dunnhumby, a data science company focused on retail food sales, released its most recent phase of its “Consumer Pulse Survey” (conducted January 25 to February 8, 2022), which revealed that U.S. consumers are less worried about COVID infections, but far more concerned about rising food prices. *

In fact, respondents to the survey are now more worried about rising food prices, the economy and their own personal finances than they are with getting COVID. Perhaps most concerning for retailers and the government is the U.S. consumers surveyed said that the food inflation rate now stands at 17.7% when it actually stands at 7.4% according to the U.S. Bureau of Labor Statistics. This last research was conducted just past the peak of the Omicron variant of the Coronavirus.

“Americans’ belief that food prices are rising more than twice as fast as they actually are should concern retailers, manufacturers and the government alike,” says Grant Steadman, president for North America at dunnhumby. “We not only see this mismatch between sentiment and reality in the U.S., but also in every country we surveyed. Consumers are now more concerned with their finances and the country’s economy than they were five months ago. We need to revise our thinking about how consumers consider inflation. Likely, we have not yet seen the full extent of how consumers will react to food price increases. This could diverge further, particularly if the security situation in Europe worsens and further impacts energy and commodity prices globally.”

Key findings of the study include the following:

- Fifty-one percent of U.S. shoppers surveyed are concerned that their money doesn’t go as far as it used to due to rising prices, marking a ten-point increase since September 2021, and a 12% increase since May 2020.

- The majority of U.S. consumers (58%) believe the economy is weak, a three-point increase from September 2021, and the same percentage from February 2021.

- Walmart was again cited for providing the best value for the money by 54% of respondents, an increase of 25 points from September 2021. Aldi (18%), Kroger (10%), and Amazon (10%) finished in the top three for best value.

- Americans’ worry about the pandemic is at an all-time low (13%) and 20 points below consumers’ worry in Chile, the country with the highest “Worry Index.”

- The surge in cases from the Omicron variant slightly reduced the number of trips consumers made to stores in late January through early February and reversed consumers’ belief from September 2021 that things were starting to return to normal. Only 19% of consumers reported that things were returning to normal in stores compared to 24% in September.

- While online shopping numbers have varied over the previous study periods, they are essentially flat from where they were in May 2020. Thirty-three percent of U.S. respondents have ordered more online since COVID-19 began. Fifty-five percent of respondents made at least one online shopping trip during the week they were surveyed, up 17% since March 2020.

- Only 39% of U.S. consumers surveyed are satisfied with the instore shopping experience, a 3% drop since September 2021. Only 36% of those surveyed felt stores are doing a good job with COVID. Although consumers’ satisfaction with how stores are addressing the virus is low, it is nearly triple the approval rate U.S. consumers have for how government has dealt with the pandemic (22%). In every country surveyed, consumers felt stores are doing a better job than the government.

- Although economic pressures have increased over the last five months, the percentage of respondents using key value-seeking strategies has remained flat (53% of respondents compared to 52% in September 2021). Value seekers see inflation rates as even higher (18.4%) than those not actively seeking value (16.9%).

This study was conducted in nine “waves” or periods as noted in the following. dunnhumby surveyed 64,827 respondents online in 23 countries: Asia (Australia, China, Japan, Malaysia, Thailand), Europe (Czechia, Denmark, France, Germany, Hungary, Ireland, Italy, Norway, Portugal, Slovakia, Spain, United Kingdom), Latin America (Brazil, Chile, Colombia and Mexico), and North America (United States, Canada). The online interviews were conducted for Wave One from March 29 - April 1 2020; Wave Two from April 11 – 14, 2020; Wave Three from May 27-31, 2020; Wave Four from July 9 – 12, 2020 in the U.S., Canada and Mexico only; Wave Five from August 28 – September 3, 2020; Wave Six from November 20 – 25, 2020; Wave 7 from February 18-24, 2021; Wave 8 from August 27 to September 3, 2021; and Wave 9 January 25, 2022 to February 8, 2022.

Approximately 400 individuals were interviewed in each country for each Wave of the study, and respondents were roughly 60% female and 40% male. The study is available as a free download.

* dunnhumby Pulse Study: Keeping our finger on the pulse of shoppers; USA Results;" “The dunnhumby Covid Consumer Pulse Survey for U.S., Wave 9 Report;” February, 2022; dunnhumby web site.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!