Supply Chain Efficiency Starts at the Top

There are many tools to make supply chains respond to quick and unplanned changes, but success must begin with senior management.

In this economy, manufacturers are challenged to find ways to maximize supply chain efficiency. Without a keen interest in defining and achieving this efficiency at the very top level of an organization, however, improved efficiency is not likely to trickle down to individual departments.

One way to gauge the importance of supply chain efficiency is to look at the organizational level of a company’s senior-most supply chain executive. “With supply chains becoming more dynamic and agile,” says Bruce Tompkins, executive director of the Tompkins Supply Chain Consortium, “companies are realizing the significance of having a high-level supply chain executive influence their business strategies.”

Nearly half of the retail and manufacturing companies surveyed by the Consortium have a supply chain leader at or above the executive vice president (EVP) level. According to the Consortium’s study, The Structure of Today’s Supply Chain Organizations, 57 percent of food and beverage processors have a supply chain leader at the EVP level, 14 percent at the senior VP level, 14 percent at the senior director level and 14 percent at the director level. Food and beverage retailers, on the other hand, realize supply chain is crucial to their operations. Consequently, 100 percent of their supply chain leaders are EVPs and up.

Supply chain efficiency, therefore, is the measure of getting the right product to the right place at the right time at the least cost. While processors want to measure their own supply chain efficiency, it’s often the customer who ultimately judges them. “Supply chain efficiency must ensure that it upholds the promise to the customer while eliminating non-value add or waste in the process,” explains Jim Stollberg, HK Systems vice president of strategy and business development.

While the five-step process generally applies to all manufacturing companies, those in the food industry face additional challenges. For example, they must also maintain traceability and manage internal resources and inventory levels in a cost-effective manner, says Manuel Pumarada, Plex Systems’ product marketing manager.

In addition, variables such as raw ingredients, packaging materials and energy affect profitability, availability and quality, says Yves Dufort, Invensys Operations Management director, food, beverage and CPG. He notes that the food industry is subjected to a number of external factors (consumer taste, income, demographics, etc.), making it necessary for the supply chain to be sensitive to, and respond to, these dynamic changes.

While supply chain efficiency involves streamlining the proactive planning of all the steps, Karin Bursa, Logility vice president of marketing, believes one more step- optimizing-should be added to the five-step list. She explains that even though many systems provide a calculator of sorts, which focuses on a single aspect of the supply chain to determine efficiency, this approach misses the opportunity to optimize the whole supply chain and identify new cost savings, including where to store inventory across each step of the manufacturing and distribution process.

Defining supply chain efficiency is at best problematic. For example, Stephen Halula, CDC Software manager of supply chain consulting, says he found 754,000 hits on Google for “supply chain efficiencies” and 50 book titles on the subject at Amazon.com. Halula likes to take what he calls a minimalist approach to the definition. He says supply chain efficiency could be viewed as:

• Providing the right product in the right quantity to a customer when desired, at a fair price with a fair margin

• Adapting to market changes

• Remaining flexible enough to accommodate problems as they are encountered, and

• Providing adequate information to all parties (customer, management, manufacturing) regarding each of the aforementioned five steps in the supply chain.

There is no end to the number of metrics that exist for supply chain performance measurement, says John Hill, TranSystems vice president. Probably the most well-known is the Perfect Order Index: an order that is delivered on time, complete, damage-free and with correct documentation. Although developed for the retail industry by the Vendor Compliance Federation, this metric is an excellent tool to identify poor and strong performance areas. Hill says metrics must be in harmony with a processor’s overall business strategy. For example, if a fresh produce supplier focused its supply chain efforts solely on delivery cost reduction, it would cripple the company’s ability to serve retailers and sustain market share.

Other metrics include inventory turns per annum, resource capitalization, improved production costs and throughput performance, service level performance, efficiency based on market responsiveness in meeting demand and introducing new products, and performance related to the time needed to execute a lot trace or manage a recall.

Two additional and very important metrics in the food industry, according to Bursa, are demand forecast accuracy, which indicates how well a processor anticipates what and when the market will buy, and how well a processor can extend freshness while a product sits on the shelf.

The $150/barrel price of oil a few years ago caused many beverage companies to overspend on transportation. Though short-lived, that price/barrel translated to $4.50 or more per gallon of gas and caused some processors to rethink strategies. For example, a brewery in the Pacific Northwest located its new facility not only near a major east-west Interstate, but also next to a railroad siding so it could ship finished brew in a southerly direction.

Weather, fuel prices and natural disasters are not the only issues that affect incoming raw ingredients. “A major problem involves the accuracy of orders of ingredients received in inventory,” says Alex Smith, managing director of Technology Group International (TGI). “Did the processor get the stuff on time, the right stuff, the exact quantity? The same thing goes for processors that use copackers or contract manufacturers.” For example, when a nutrition bar company tells its copacker it needs so many cases of the product shipped right away, the reality is the nutrition bar company already has an order from one of its customers.

Another example Smith notes is a TGI customer that produces sausages and bratwurst. There are times when the processor might order 50,000 lbs. of pork and receive only 10,000 lbs., or on another occasion, it might receive 70,000 lbs. for a 50,000-lb. order. While an inaccurate order of this magnitude isn’t a problem in most segments of the food industry, it’s a major problem in the area of processed meats where it occurs on a frequent basis, according to Smith.

Forecasting market demand presents yet another challenge. “Many food companies base their demand and purchase planning on last year’s sales,” says Mikael Anden, Lawson vice president. While this is often a good starting point, demand can be influenced by changes in key customers, promotions, weather, product introductions, etc. Key account managers can normally provide significant market intelligence to improve forecast and drive planning accuracy.

Seasonal demands create additional challenges in forecasting market demand. Extra soda and beer for July 4th and turkeys for Thanksgiving are prime examples, says Halula. He sees the need to keep the product in a proper environment (refrigerated, frozen, upright, not overheated) to preserve freshness as another weak link in supply chain efficiency.

Pumarada, on the other hand, sees traceability beyond the first supplier tier as the weakest link. Increasingly complex products drive greater dependency on supplier quality management, and therefore, documenting quality and processes through every step of the supply chain is necessary.

Assuming suppliers do have a traceability and quality documentation program in place, yet another weak link is the incompatibility of software systems used among those participating in the supply chain, says Chad Collins, HighJump Software’s vice president of marketing and strategy. Plus, when a processor has information from its ingredient suppliers, it may not be documenting the steps in its own processes-or if it is documenting the steps, the documentation is on paper.

In the food industry, many processing steps can’t be automated and require operator intervention. These are often the steps that escape documentation, says Jonathan Lustri, Emerson Process Management Syncade brand manager, even though tools exist to allow an electronically documented, step-by-step procedure of all manually operated steps. This documentation can then be added to the overall traceability information on the product so the next customer in the supply chain has access to these records. Lustri adds that more processors expect at least this kind of documentation on their incoming ingredients.

Finally, processors need to realize the food and beverage supply chain is not the same as the supply chain of other retail products. “I believe the weakest link can vary depending upon company and situation,” says Stollberg. “One company may be very efficient at planning but poor at manufacturing; another may have the opposite scenario. While each will have its own core competencies, the company that understands how to manage the holistic view will be most efficient. While I’m not sure I’d call it a weak link, what is a unique characteristic of the food/beverage supply chain is that it is human consumable. This requires added safety, security and quality measures that other supply chains may not have.”

Besides long lead times-anywhere from two to five weeks or more when products are shipped from South America or China-globalization brings related challenges, says Collins. While in transit, has the product been stored at the proper temperature and humidity? Can the products be traced through the various stages of growing to manufacturing? If there is a certificate of authenticity, is it real and valid?

The weaknesses built into the globalization model are many and complex, says Wulfraat. The list includes political stability, currency valuation, inflation rates, intellectual property rights, quality control, lead times, volatile transportation costs, inbound delays and disruptions, and poor supply chain visibility.

Planning, organizing and executing transportation has always been a challenge, but right now it’s a greater challenge. The reason, according to Tompkins, is the lack of capacity. At first it could be blamed on higher fuel costs. But Tompkins believes the current lack of capacity is a direct result of the recession-where many smaller and medium-sized trucking companies woke up and found themselves out of business as manufacturers cut back or went out of business. It takes time to rebuild capacity, and it won’t happen overnight. Tompkins says it’s not only trucking that was hit; other modes of transportation saw cutbacks as well. The result: higher transportation costs and less availability.

Most food and beverage processors have made efforts to navigate these troubled waters through better planning, execution and analytics, says John Blanchard, TranSystems senior consultant. “The degree to which discrete cost components are managed is what will separate the good from the great as fuel prices and other factors like regulatory compliance and capacity management apply upward pressure on transportation costs,” he adds.

Processors who need a little help in reducing fuel consumption and emissions can get involved with the EPA Smartway program, says Jason Mathers, Environmental Defense Fund project manager. Many food and beverage companies already participate in the program, including Chiquita Brands International, General Mills, Kellogg Company, Mars Snackfood, MillerCoors, Ocean Spray and Sara Lee. Mathers points out the success Walmart has achieved in improving fleet operations: a 60 percent increase in fleet efficiency, delivering 77 million more cases in 2009 than in 2008 while eliminating more than 100 million miles.

Optimizing routes so trucks are filled in both directions can make a difference for processors with their own fleets. But there may be other solutions for saving money on transportation, suggests Blanchard. Organizations that have already deployed software tools to optimize their internal transportation should look outside for incremental improvements. Selling capacity to other organizations, even competitors, is a largely untapped method of achieving better utilization.

A key solution to the transportation dilemma (what the top 20 percent of companies are using) is logistics software tools that apply the most efficient rates and shortest routes to the destination, says Rene Inzana, Syspro product manager. These tools adjust routes and delivery loads to maximize the amount of goods shipped per mile.

For processors that may not have transportation management system (TMS) and warehouse management system (WMS) tools, another option may be outsourcing all shipping to logistical service providers (LSPs), says Tompkins. LSPs can effectively manage warehouses and handle shipping and scheduling.

To minimize transportation costs, some processors are planning their locations very smartly. Jeffery Goh, CEO of Two Chefs on a Roll, says its Carson, CA plant grew to a size where he knew it would be more practical to locate another facility on the East Coast. Its new location near Scranton in northeastern Pennsylvania offers easy access to markets in the New England and Mid-Atlantic states.

Goh believes the best way to create a highly efficient distribution system is to plan “micro-plants” close to the customer base. With a micro-plant, Goh outsources storage and shipping because LSPs do a better job, which allows his staff to focus on creating and making product.

Goh goes directly to the grower as often as he can. He contracts hundreds of acres of crops, walks the fields and guarantees purchase. If he has a surplus, he puts it out to market at a profit. The point Goh makes is that processors must learn how to drive costs out of the system-and that requires understanding the complete distribution system-from grower to the final customer, whether it’s a restaurant or the consumer.

Technology can help processors get some control over incoming produce from farms and growers. According to Hill, many of the same tools and systems used by major food producers for managing material and data flow within their facilities and in transit to customers hold equal potential for managing the flow from field or farm to the processing plant. For example, the use of electronic scales and embedded RFID tags for license-plating raw produce containers would enable growers to weigh, identify, create accurate shipping documentation and transmit actual shipment data to processors as trailers leave the farm.

On receipt at the plant, tags could be read and containers weighed to verify shipment content and drive subsequent processing. Oftentimes, the challenge for growers, particularly independents, has to do with the level of investment required for implementation of the required technology and systems infrastructure. A possible solution might be financial support from processors for whom potential benefits are significant, adds Hill.

Agricultural solutions to address planting, growing, harvesting, chemical application, irrigation and grower management are becoming available within several ERP applications, says Johann Heydenrych, itelligence Group director of industry solutions. One example is itelligence’s myAgri, a qualified SAP Business All-in-One partner solution.

Companies operating in meat, poultry, dairy and other food segments often need to manage raw materials, or finished products, with variable weight (also known as catch weight), says Anden. Ordering and logistics are often performed in a logistical unit, while financial transactions need to be driven by a parallel weight-based unit. Software is available to provide catch weight information down to the individual package, or stock balance ID, which is paired with end-to-end support for catch weight-based pricing, costing and inventory valuation. This enables a processor to work with detailed catch weight information across the supply chain and measure a true weight-based margin.

Yield optimization of material usage is another area that has the potential to significantly improve the bottom line for food manufacturers. In meat, poultry and fish processing as well as in fruit and vegetable canning and freezing, raw ingredients have variable grades. Maximum yield and profitability are dependent on the allocation of raw materials and ingredients, as well as the selection of processing methods to balance supply and demand in the most cost-effective manner, adds Anden.

While it’s difficult to predict natural disasters or to gauge when political relations could threaten ingredient purchases, food processors face daily challenges in the supply chain. Processors that fail to make the supply chain a high-level priority corporate strategy will find themselves quickly losing their competitive edge.

For more information:

Jim Stollberg, HK Systems Inc., 262-860-6558

Manuel Pumarada, Plex Systems, 248-391-8001, mpumarada@plex.com

Karin Bursa, Logility, 800-762-5207, kbursa@logility.com

Stephen Halula, CDC Software, 800-236-4600, shalula@cdcsoftware.com

Rene Inzana, Syspro, 714-437-1000, rene.inzana@us.syspro.com

Mark Wulfraat, MWPVL International Inc., 514-482-3572, info@mwpvl.com

Mikael Anden, Lawson, 847-762-0900, mikael.anden@us.lawson.com

Alex Smith, Technology Group International, 800-837-0028

Chad Collins, HighJump Software, 952-947-4088, chad.collins@highjump.com

Jonathan Lustri, Emerson Process Management, 512-832-3279

John Hill, TranSystems, 800-800-5261

John Blanchard, TranSystems, 800-800-5261

Jason Mathers, Environmental Defense Fund, 617-406-1806, jmathers@edf.org

Johann Heydenrych, itelligence, 513-956-2000, johann.heydenrych@itelligencegroup.com

Bruce Tompkins, Tompkins Supply Chain Consortium, 919-876-3667

Yves Dufort, Invensys Operations Management, 514-421-5135, yves.dufort@invensys.com

But physical improvements weren’t enough. The company had 70 route drivers delivering direct to store using manual, paper-based processes, which proved to be inefficient. Management knew it was time to invest in technology if the company were to continue to meet increasing customer demands.

“In an effort to grow our customer base, we took on bigger, more sophisticated customers, and started receiving requirements to deliver farther and farther away,” says Steve Feldkamp, chief operations officer.

The dairy implemented HighJump Route Administrator and Route Assistant software. The Route Administrator DSD route accounting system creates the backbone of Umpqua operations. The software manages the company’s routes, handheld computing devices and customer and driver schedules, in addition to controlling the integration with the dairy’s ERP system.

“The route drivers like the new system and are becoming more efficient, completing their routes faster and finding time for additional stops,” says Feldkamp. “We have also been able to eliminate the paper-based processes associated with entering orders and invoices and correcting mistakes manually. This has been a critical factor in preparing us for continued growth,” he adds.

“Overall, HighJump Route Administrator and Route Assistant have allowed us to grow our business while increasing efficiency,” says Feldkamp. “On top of that, our customers are happier. And that’s really what it’s all about.”

The report found that products from local farms are marketed through both mainstream and local supply chains, and products from mainstream and local supply chains may be present in the same retail outlet. Despite generally higher per unit costs than mainstream chains, farms and businesses can still be successful if they offer unique product characteristics or services, diversify their operations and have access to process and distribution services.

Local food supply chains, particularly direct market (producer-to-consumer) chains are more likely than mainstream chains to provide consumers with detailed information about where and by whom products were produced, but such information generally is not enough to persuade consumers to pay a higher price for local food products. Product differentiation based on other attributes such as organic or grass-fed production appear to be primary influences on prices in local supply chains, says the report.

Other findings include:

• Local food supply chains tend to have a diverse portfolio of products and market outlets.

• The local chains have adequate access to processing and distribution services.

• Producers receive a greater share of retail prices in local supply chains than they do in mainstream supply chains.

• Nearly all wage and proprietor income in the local supply chains is retained locally, but local areas also retain a large share of wage and proprietor income from the mainstream supply chains.

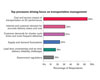

Among transportation executives, the focus on improving the role of transportation in the supply chain has continued to grow since the report was launched in 2007, when only 54 percent felt transportation had the greatest impact on supply chain performance. Source: Aberdeen Group.

In this economy, manufacturers are challenged to find ways to maximize supply chain efficiency. Without a keen interest in defining and achieving this efficiency at the very top level of an organization, however, improved efficiency is not likely to trickle down to individual departments.

One way to gauge the importance of supply chain efficiency is to look at the organizational level of a company’s senior-most supply chain executive. “With supply chains becoming more dynamic and agile,” says Bruce Tompkins, executive director of the Tompkins Supply Chain Consortium, “companies are realizing the significance of having a high-level supply chain executive influence their business strategies.”

Nearly half of the retail and manufacturing companies surveyed by the Consortium have a supply chain leader at or above the executive vice president (EVP) level. According to the Consortium’s study, The Structure of Today’s Supply Chain Organizations, 57 percent of food and beverage processors have a supply chain leader at the EVP level, 14 percent at the senior VP level, 14 percent at the senior director level and 14 percent at the director level. Food and beverage retailers, on the other hand, realize supply chain is crucial to their operations. Consequently, 100 percent of their supply chain leaders are EVPs and up.

Voice-directed picking improves safety by eliminating the use of handheld devices and increases efficiency in this Performance Food Group (PFG) warehouse. PFG markets and distributes more than 68,000 national and private-label food and food-related products to more than 41,000 restaurants and institutional customers across the US. Voice software from Voxware works in conjunction with existing WMS systems and helped PFG achieve 99.96 percent pick accuracy with a 50 percent reduction in truck shorts. Voxware can be used with or without handheld barcode and RFID devices. Source: Voxware.

Defining supply chain efficiency

Very simply put, a supply chain is a system of organizations, resources, activities, people, information and technology involved in moving a product from a supplier to a customer. Any manufacturer or producer typically performs five steps in the supply chain: planning, sourcing (finding suppliers), making (manufacturing), delivering and returning (taking back defective goods).Supply chain efficiency, therefore, is the measure of getting the right product to the right place at the right time at the least cost. While processors want to measure their own supply chain efficiency, it’s often the customer who ultimately judges them. “Supply chain efficiency must ensure that it upholds the promise to the customer while eliminating non-value add or waste in the process,” explains Jim Stollberg, HK Systems vice president of strategy and business development.

While the five-step process generally applies to all manufacturing companies, those in the food industry face additional challenges. For example, they must also maintain traceability and manage internal resources and inventory levels in a cost-effective manner, says Manuel Pumarada, Plex Systems’ product marketing manager.

In addition, variables such as raw ingredients, packaging materials and energy affect profitability, availability and quality, says Yves Dufort, Invensys Operations Management director, food, beverage and CPG. He notes that the food industry is subjected to a number of external factors (consumer taste, income, demographics, etc.), making it necessary for the supply chain to be sensitive to, and respond to, these dynamic changes.

While supply chain efficiency involves streamlining the proactive planning of all the steps, Karin Bursa, Logility vice president of marketing, believes one more step- optimizing-should be added to the five-step list. She explains that even though many systems provide a calculator of sorts, which focuses on a single aspect of the supply chain to determine efficiency, this approach misses the opportunity to optimize the whole supply chain and identify new cost savings, including where to store inventory across each step of the manufacturing and distribution process.

Defining supply chain efficiency is at best problematic. For example, Stephen Halula, CDC Software manager of supply chain consulting, says he found 754,000 hits on Google for “supply chain efficiencies” and 50 book titles on the subject at Amazon.com. Halula likes to take what he calls a minimalist approach to the definition. He says supply chain efficiency could be viewed as:

• Providing the right product in the right quantity to a customer when desired, at a fair price with a fair margin

• Adapting to market changes

• Remaining flexible enough to accommodate problems as they are encountered, and

• Providing adequate information to all parties (customer, management, manufacturing) regarding each of the aforementioned five steps in the supply chain.

Metrics for efficiency

Supply chain efficiency metrics compare all costs incurred to move product and information from the source to the customer to the processor’s ability to meet its turnaround targets, says Marc Wulfraat, MWPVL International president. The costs to be tallied include inbound freight, inter-facility transfers, outbound freight, production and warehouse operating expenses. In addition, the costs of inventory assets and working capital invested in inventory and infrastructure need to be included. The goal is to minimize the cost of operating expenses and working capital required to meet customer delivery (service level) commitments. Accordingly, he adds, service level objectives play a major role in framing a company’s supply chain infrastructure.There is no end to the number of metrics that exist for supply chain performance measurement, says John Hill, TranSystems vice president. Probably the most well-known is the Perfect Order Index: an order that is delivered on time, complete, damage-free and with correct documentation. Although developed for the retail industry by the Vendor Compliance Federation, this metric is an excellent tool to identify poor and strong performance areas. Hill says metrics must be in harmony with a processor’s overall business strategy. For example, if a fresh produce supplier focused its supply chain efforts solely on delivery cost reduction, it would cripple the company’s ability to serve retailers and sustain market share.

Other metrics include inventory turns per annum, resource capitalization, improved production costs and throughput performance, service level performance, efficiency based on market responsiveness in meeting demand and introducing new products, and performance related to the time needed to execute a lot trace or manage a recall.

Two additional and very important metrics in the food industry, according to Bursa, are demand forecast accuracy, which indicates how well a processor anticipates what and when the market will buy, and how well a processor can extend freshness while a product sits on the shelf.

While food and beverage processors don’t have the greatest number of supply chain leaders at executive vice president levels and above compared to other manufacturers, food and beverage retailers realize the importance of having supply chain leaders at the highest executive levels. Source: Tompkins Supply Chain Consortium.

What is the weakest link?

A supply chain is only as good as its weakest link. “For most companies, the weakest links are those they cannot control,” says Wulfraat. “These most commonly have to do with the sources of supply of raw materials. Sudden and unexpected events can cause extreme supply shortages for commodities that in turn cause major price increases.” While weather can always be an issue affecting incoming ingredients, other shocks can include oil spills that harm the supply of seafood and rapid escalation of oil prices that can overrun transportation budgets.The $150/barrel price of oil a few years ago caused many beverage companies to overspend on transportation. Though short-lived, that price/barrel translated to $4.50 or more per gallon of gas and caused some processors to rethink strategies. For example, a brewery in the Pacific Northwest located its new facility not only near a major east-west Interstate, but also next to a railroad siding so it could ship finished brew in a southerly direction.

Weather, fuel prices and natural disasters are not the only issues that affect incoming raw ingredients. “A major problem involves the accuracy of orders of ingredients received in inventory,” says Alex Smith, managing director of Technology Group International (TGI). “Did the processor get the stuff on time, the right stuff, the exact quantity? The same thing goes for processors that use copackers or contract manufacturers.” For example, when a nutrition bar company tells its copacker it needs so many cases of the product shipped right away, the reality is the nutrition bar company already has an order from one of its customers.

Another example Smith notes is a TGI customer that produces sausages and bratwurst. There are times when the processor might order 50,000 lbs. of pork and receive only 10,000 lbs., or on another occasion, it might receive 70,000 lbs. for a 50,000-lb. order. While an inaccurate order of this magnitude isn’t a problem in most segments of the food industry, it’s a major problem in the area of processed meats where it occurs on a frequent basis, according to Smith.

Forecasting market demand presents yet another challenge. “Many food companies base their demand and purchase planning on last year’s sales,” says Mikael Anden, Lawson vice president. While this is often a good starting point, demand can be influenced by changes in key customers, promotions, weather, product introductions, etc. Key account managers can normally provide significant market intelligence to improve forecast and drive planning accuracy.

Seasonal demands create additional challenges in forecasting market demand. Extra soda and beer for July 4th and turkeys for Thanksgiving are prime examples, says Halula. He sees the need to keep the product in a proper environment (refrigerated, frozen, upright, not overheated) to preserve freshness as another weak link in supply chain efficiency.

Pumarada, on the other hand, sees traceability beyond the first supplier tier as the weakest link. Increasingly complex products drive greater dependency on supplier quality management, and therefore, documenting quality and processes through every step of the supply chain is necessary.

Assuming suppliers do have a traceability and quality documentation program in place, yet another weak link is the incompatibility of software systems used among those participating in the supply chain, says Chad Collins, HighJump Software’s vice president of marketing and strategy. Plus, when a processor has information from its ingredient suppliers, it may not be documenting the steps in its own processes-or if it is documenting the steps, the documentation is on paper.

In the food industry, many processing steps can’t be automated and require operator intervention. These are often the steps that escape documentation, says Jonathan Lustri, Emerson Process Management Syncade brand manager, even though tools exist to allow an electronically documented, step-by-step procedure of all manually operated steps. This documentation can then be added to the overall traceability information on the product so the next customer in the supply chain has access to these records. Lustri adds that more processors expect at least this kind of documentation on their incoming ingredients.

Finally, processors need to realize the food and beverage supply chain is not the same as the supply chain of other retail products. “I believe the weakest link can vary depending upon company and situation,” says Stollberg. “One company may be very efficient at planning but poor at manufacturing; another may have the opposite scenario. While each will have its own core competencies, the company that understands how to manage the holistic view will be most efficient. While I’m not sure I’d call it a weak link, what is a unique characteristic of the food/beverage supply chain is that it is human consumable. This requires added safety, security and quality measures that other supply chains may not have.”

Globalization-asset or liability?

Globalization presents both opportunities and challenges, says Stollberg. Many processors have struggled with sourcing products from countries where labor is cheap and ingredient costs are lower, yet planning and transportation are complicated. Therefore, processors need to consider the impact of total cycle time and cost based on these complexities.Besides long lead times-anywhere from two to five weeks or more when products are shipped from South America or China-globalization brings related challenges, says Collins. While in transit, has the product been stored at the proper temperature and humidity? Can the products be traced through the various stages of growing to manufacturing? If there is a certificate of authenticity, is it real and valid?

The weaknesses built into the globalization model are many and complex, says Wulfraat. The list includes political stability, currency valuation, inflation rates, intellectual property rights, quality control, lead times, volatile transportation costs, inbound delays and disruptions, and poor supply chain visibility.

Taming transportation

According to a study from the Aberdeen Group, Integrated Transportation Management: Improve Responsiveness with Real-Time Control of Execution, best-in-class companies (the top 20 percent of performers) have a spend ratio of 2.93 percent, i.e., transportation costs divided by sales. With an emphasis on real-time visibility and control of their supply chains, these companies have actually seen a 4.44 percent improvement in transportation costs over the prior year. In addition, they averaged 98.6 percent on-time and complete shipments and are 2.3 times more likely than all other companies to measure performance weekly or more often. These top performers are 1.3 times more likely to use supply chain visibility software.Planning, organizing and executing transportation has always been a challenge, but right now it’s a greater challenge. The reason, according to Tompkins, is the lack of capacity. At first it could be blamed on higher fuel costs. But Tompkins believes the current lack of capacity is a direct result of the recession-where many smaller and medium-sized trucking companies woke up and found themselves out of business as manufacturers cut back or went out of business. It takes time to rebuild capacity, and it won’t happen overnight. Tompkins says it’s not only trucking that was hit; other modes of transportation saw cutbacks as well. The result: higher transportation costs and less availability.

Most food and beverage processors have made efforts to navigate these troubled waters through better planning, execution and analytics, says John Blanchard, TranSystems senior consultant. “The degree to which discrete cost components are managed is what will separate the good from the great as fuel prices and other factors like regulatory compliance and capacity management apply upward pressure on transportation costs,” he adds.

Processors who need a little help in reducing fuel consumption and emissions can get involved with the EPA Smartway program, says Jason Mathers, Environmental Defense Fund project manager. Many food and beverage companies already participate in the program, including Chiquita Brands International, General Mills, Kellogg Company, Mars Snackfood, MillerCoors, Ocean Spray and Sara Lee. Mathers points out the success Walmart has achieved in improving fleet operations: a 60 percent increase in fleet efficiency, delivering 77 million more cases in 2009 than in 2008 while eliminating more than 100 million miles.

Optimizing routes so trucks are filled in both directions can make a difference for processors with their own fleets. But there may be other solutions for saving money on transportation, suggests Blanchard. Organizations that have already deployed software tools to optimize their internal transportation should look outside for incremental improvements. Selling capacity to other organizations, even competitors, is a largely untapped method of achieving better utilization.

A key solution to the transportation dilemma (what the top 20 percent of companies are using) is logistics software tools that apply the most efficient rates and shortest routes to the destination, says Rene Inzana, Syspro product manager. These tools adjust routes and delivery loads to maximize the amount of goods shipped per mile.

For processors that may not have transportation management system (TMS) and warehouse management system (WMS) tools, another option may be outsourcing all shipping to logistical service providers (LSPs), says Tompkins. LSPs can effectively manage warehouses and handle shipping and scheduling.

To minimize transportation costs, some processors are planning their locations very smartly. Jeffery Goh, CEO of Two Chefs on a Roll, says its Carson, CA plant grew to a size where he knew it would be more practical to locate another facility on the East Coast. Its new location near Scranton in northeastern Pennsylvania offers easy access to markets in the New England and Mid-Atlantic states.

Goh believes the best way to create a highly efficient distribution system is to plan “micro-plants” close to the customer base. With a micro-plant, Goh outsources storage and shipping because LSPs do a better job, which allows his staff to focus on creating and making product.

Managing the supply side

If only processors could get more control of incoming ingredients. That’s one big “if” that has plagued many food manufacturers over the years. To address this problem, some processors move to a vertical model where they either grow their own ingredients or protect themselves by hedging or buying forward contracts, says Dufort. “The biggest advantage in using a vertical or integrated business model is control. However, the risk in integrating activities is losing core competencies, having to stretch resources and, for example, potentially having to rely on older or inadequate technology,” he adds.Goh goes directly to the grower as often as he can. He contracts hundreds of acres of crops, walks the fields and guarantees purchase. If he has a surplus, he puts it out to market at a profit. The point Goh makes is that processors must learn how to drive costs out of the system-and that requires understanding the complete distribution system-from grower to the final customer, whether it’s a restaurant or the consumer.

Technology can help processors get some control over incoming produce from farms and growers. According to Hill, many of the same tools and systems used by major food producers for managing material and data flow within their facilities and in transit to customers hold equal potential for managing the flow from field or farm to the processing plant. For example, the use of electronic scales and embedded RFID tags for license-plating raw produce containers would enable growers to weigh, identify, create accurate shipping documentation and transmit actual shipment data to processors as trailers leave the farm.

On receipt at the plant, tags could be read and containers weighed to verify shipment content and drive subsequent processing. Oftentimes, the challenge for growers, particularly independents, has to do with the level of investment required for implementation of the required technology and systems infrastructure. A possible solution might be financial support from processors for whom potential benefits are significant, adds Hill.

Agricultural solutions to address planting, growing, harvesting, chemical application, irrigation and grower management are becoming available within several ERP applications, says Johann Heydenrych, itelligence Group director of industry solutions. One example is itelligence’s myAgri, a qualified SAP Business All-in-One partner solution.

Companies operating in meat, poultry, dairy and other food segments often need to manage raw materials, or finished products, with variable weight (also known as catch weight), says Anden. Ordering and logistics are often performed in a logistical unit, while financial transactions need to be driven by a parallel weight-based unit. Software is available to provide catch weight information down to the individual package, or stock balance ID, which is paired with end-to-end support for catch weight-based pricing, costing and inventory valuation. This enables a processor to work with detailed catch weight information across the supply chain and measure a true weight-based margin.

Yield optimization of material usage is another area that has the potential to significantly improve the bottom line for food manufacturers. In meat, poultry and fish processing as well as in fruit and vegetable canning and freezing, raw ingredients have variable grades. Maximum yield and profitability are dependent on the allocation of raw materials and ingredients, as well as the selection of processing methods to balance supply and demand in the most cost-effective manner, adds Anden.

While it’s difficult to predict natural disasters or to gauge when political relations could threaten ingredient purchases, food processors face daily challenges in the supply chain. Processors that fail to make the supply chain a high-level priority corporate strategy will find themselves quickly losing their competitive edge.

For more information:

Jim Stollberg, HK Systems Inc., 262-860-6558

Manuel Pumarada, Plex Systems, 248-391-8001, mpumarada@plex.com

Karin Bursa, Logility, 800-762-5207, kbursa@logility.com

Stephen Halula, CDC Software, 800-236-4600, shalula@cdcsoftware.com

Rene Inzana, Syspro, 714-437-1000, rene.inzana@us.syspro.com

Mark Wulfraat, MWPVL International Inc., 514-482-3572, info@mwpvl.com

Mikael Anden, Lawson, 847-762-0900, mikael.anden@us.lawson.com

Alex Smith, Technology Group International, 800-837-0028

Chad Collins, HighJump Software, 952-947-4088, chad.collins@highjump.com

Jonathan Lustri, Emerson Process Management, 512-832-3279

John Hill, TranSystems, 800-800-5261

John Blanchard, TranSystems, 800-800-5261

Jason Mathers, Environmental Defense Fund, 617-406-1806, jmathers@edf.org

Johann Heydenrych, itelligence, 513-956-2000, johann.heydenrych@itelligencegroup.com

Bruce Tompkins, Tompkins Supply Chain Consortium, 919-876-3667

Yves Dufort, Invensys Operations Management, 514-421-5135, yves.dufort@invensys.com

Dairy automates transportation scheduling

Located in Roseburg, OR, Umpqua Dairy evolved from a small ice house with a 1929 Hudson delivery truck and grew into a multi-state operation with 70 route drivers. To keep up with sales growth, the company invested in supporting infrastructure as necessary, including new distribution centers, packaging equipment and delivery trucks.But physical improvements weren’t enough. The company had 70 route drivers delivering direct to store using manual, paper-based processes, which proved to be inefficient. Management knew it was time to invest in technology if the company were to continue to meet increasing customer demands.

“In an effort to grow our customer base, we took on bigger, more sophisticated customers, and started receiving requirements to deliver farther and farther away,” says Steve Feldkamp, chief operations officer.

The dairy implemented HighJump Route Administrator and Route Assistant software. The Route Administrator DSD route accounting system creates the backbone of Umpqua operations. The software manages the company’s routes, handheld computing devices and customer and driver schedules, in addition to controlling the integration with the dairy’s ERP system.

“The route drivers like the new system and are becoming more efficient, completing their routes faster and finding time for additional stops,” says Feldkamp. “We have also been able to eliminate the paper-based processes associated with entering orders and invoices and correcting mistakes manually. This has been a critical factor in preparing us for continued growth,” he adds.

“Overall, HighJump Route Administrator and Route Assistant have allowed us to grow our business while increasing efficiency,” says Feldkamp. “On top of that, our customers are happier. And that’s really what it’s all about.”

Local supply chains are alive and well

Demand for locally produced food has increased sharply in recent years, according to a report from USDA’s Economic Research Service of the USDA. The report, Comparing the Structure, Size, and Performance of Local and Mainstream Food Supply Chains, says local foods are increasingly incorporated in programs designed to reduce food insecurity, support small farmers and rural economies, encourage more healthful eating habits and foster closer connections between farmers and consumers.The report found that products from local farms are marketed through both mainstream and local supply chains, and products from mainstream and local supply chains may be present in the same retail outlet. Despite generally higher per unit costs than mainstream chains, farms and businesses can still be successful if they offer unique product characteristics or services, diversify their operations and have access to process and distribution services.

Local food supply chains, particularly direct market (producer-to-consumer) chains are more likely than mainstream chains to provide consumers with detailed information about where and by whom products were produced, but such information generally is not enough to persuade consumers to pay a higher price for local food products. Product differentiation based on other attributes such as organic or grass-fed production appear to be primary influences on prices in local supply chains, says the report.

Other findings include:

• Local food supply chains tend to have a diverse portfolio of products and market outlets.

• The local chains have adequate access to processing and distribution services.

• Producers receive a greater share of retail prices in local supply chains than they do in mainstream supply chains.

• Nearly all wage and proprietor income in the local supply chains is retained locally, but local areas also retain a large share of wage and proprietor income from the mainstream supply chains.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!