Manufacturing News

COVID-19 hits meat and beverage hard

Report tracks how plants closures, shortages impact retail shelves and industry's future stability

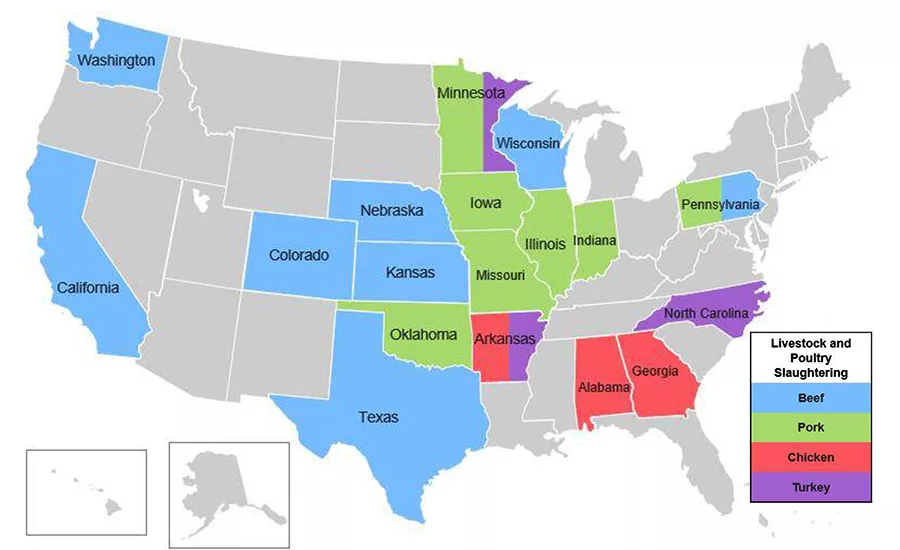

States with a majority of slaughtering facilities in the U.S. faced several worker shortages during the COVID-19 pandemic.

Chart courtesy of Resilience360/Meatinstitute.org

Most consumers have seen the results of COVID-19 when attempting to purchase meat at the local grocery—high prices and limits on purchases.

On average, meat processing and packaging plants were closed for about 11 days, with 44% of all closures lasting up to 14 days and 28% lasting 15 days or more, according to a report, “The COVID-19 Pandemic Disrupts Food and Beverage Supply Chains in the U.S.,” from the Resilience360 supply chain platform. The most affected plants are owned by Tyson Foods, JBS, Hormel and Cargill, located in leading meat processing states: Iowa, Minnesota, Pennsylvania, Indiana and Illinois.

Resilience360 predicts, monitors and mitigates supply chain disruptions—both man-made and natural, including hurricanes, cyberattacks, labor strikes and protests.

As a result of COVID-19 disruptions, the meat industry could face losses of up to $20 billion. The industry has seen more than 20,000 workers become infected, and the downward spiral of purchases by restaurants and schools has further hurt the industry. The related plant closures have pushed wholesale prices up and decreased livestock prices, which began to normalize in mid-May.

According to the Bureau of Labor Statistics, grocery prices jumped 2.6% in April, making it the largest one-month increase since 1974. Beef prices reportedly increased by 3.3%, pork by 3% and chicken by 5.8%. Processed meat, such as hot dogs, saw a 5.7% increase.

Meats were not the only product area affected, the Resilience360 report says. Beverage and food manufacturers have also been exposed to other challenges stemming from the pandemic. For example, a shortage of carbon dioxide due to lowered ethanol production levels resulted in higher CO2 rates and associated disruption to beer and soda manufacturers. CO2 is a byproduct of the ethanol process, which also experienced labor interruptions.

Products most affected by the CO2 decrease in availability include beer, soda and seltzer, as well as fresh and preserved foods from manufacturers who rely on a steady supply of CO2. The study suggests that CO2 production is likely to fall further to 50%, following an already recorded 20% reduction. To cope with the CO2 shortage, manufacturers had to increase on-site storage capacity, find alternatives such as nitrogen or switch to other available suppliers, which have also led to higher costs and unplanned supply challenges.

Back in business … sort of

While a majority of meat processing and packaging plants have already opened and resumed operations at reduced capacity, mid- to long-term impacts can be expected, says the report. Temporary food shortages, especially for meat and other processed products and beverages, are likely but remain open to a rapid recovery with operations up and running again. Price increases and limited selection in supermarkets are likely to be seen in the coming weeks. The industry is likely to face long-term challenges in neutralizing the disruptions experienced during the pandemic.

Overall, the U.S. domestic supply chain demonstrated resiliency during the worst of the pandemic in the second quarter, albeit with reverberations in retail and occupational health and safety areas. The long-term effects, however, remain to be seen beyond the second quarter economic results and the retail impacts. The possibilities for a future disruption of food supply chains remain in the event of a COVID-19 resurgence.

The study also points out that logistical bottlenecks may still persist, which means shippers will have to be ready to adapt to changes internationally.

For more information, visit www.resilience360.dhl.com.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!